More than halfway through 2018, the mobile phone market is as busy as ever, without pre-heating marketing of ordinary roads, and the e-commerce war of gunpowder is almost uninterrupted. Although the reports given by IDC, Gartner, etc. all point to the fact that the Chinese mobile phone market has continued to weaken, it also limits the growth potential of major mobile phone brands.

The reason is not difficult to understand. According to China Mobile's plan, 5G commercialization will be promoted in some regions in 2018. In 2019, more than 1 million 4G base stations in China will be updated to 5G... The transition from 4G to 5G era will follow There is also a new wave of change, and all major mobile phone manufacturers are waiting for it.

Can 5G really become a new watershed in the mobile phone market? The market dividend is only one of them, and the user behavior is the second. Weibo and Sino has just released the "Smart Phone Micro Report 2017", the biggest difference is the interpretation of the trend of the mobile phone market from the perspective of user behavior. From this perspective, the upcoming 5G era is a national dividend, or an unfavorable factor in accelerating the siphon effect. There seems to be some answers beyond conventional cognition.

Where does the user come from and where will it flow?

After entering 2016, the domestic mobile phone market has repeatedly been mentioned as “stock changeâ€. As the name suggests, the domestic mobile phone market is nearing saturation, and the growth of one brand means the decline of another brand. Many third-party reports reveal the T-shaped pattern of the mobile phone market, that is, the top five mobile phone brands have taken over 80% of the market share, but the "Smart Phone Micro Report" focusing on user behavior gives a more detailed answer. :

1, subtle user change machine flow. The biggest attraction of stock competition is undoubtedly the source of new users' inflows, and to some extent reflects the competitiveness of competitors.

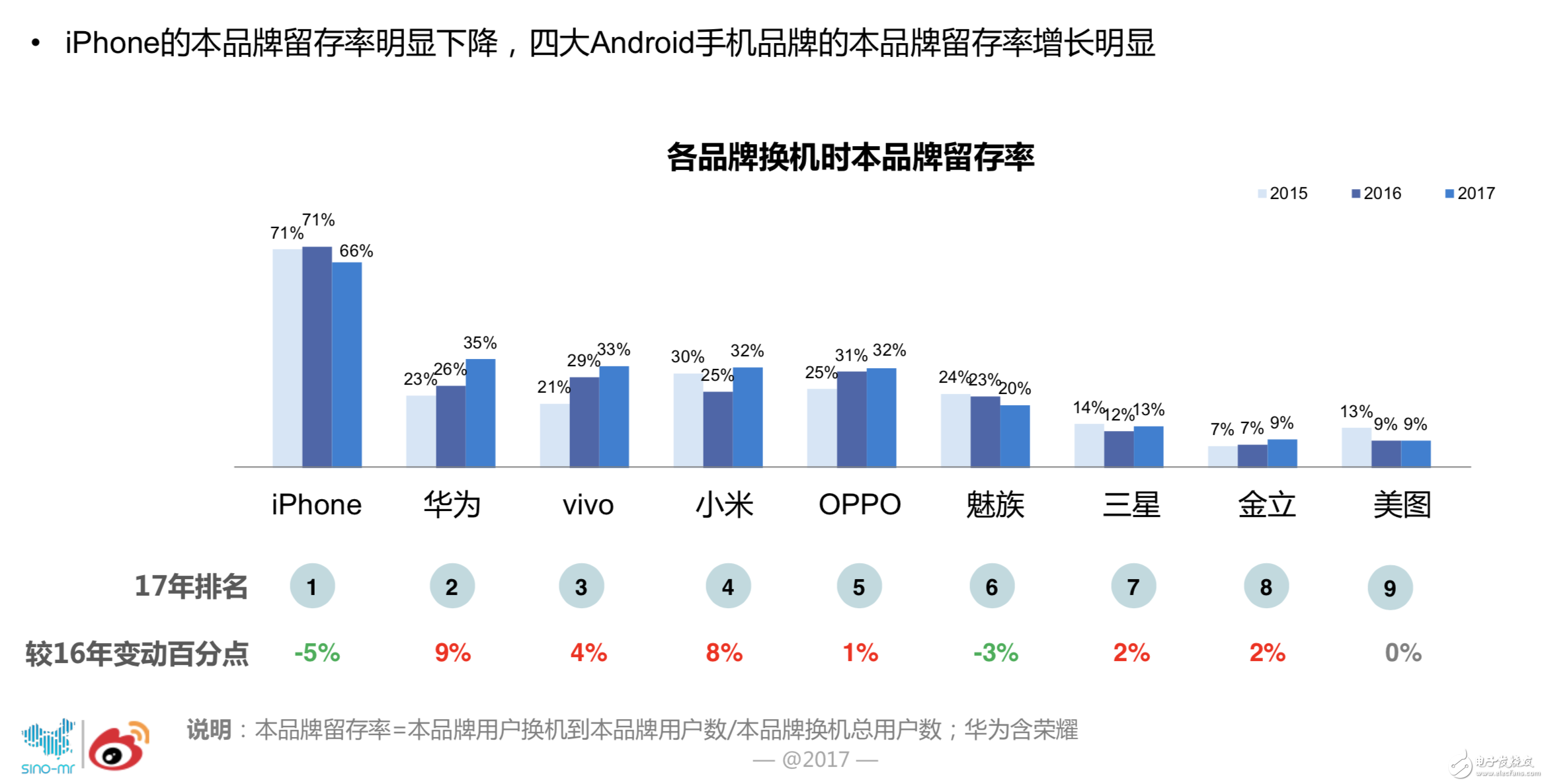

In the iPhone and iPhone 8 inflow sources, the brand accounted for 91% and 73% respectively, while OPPO, vivo, Huawei, Xiaomi, and glory, etc., accounted for 25%-39 users from the brand. Between the %, the proportion from the iPhone is generally around 20%. It is true that Apple still has the loyalty of the Android brand, but the iPhone has also lost its Android market, which proves the feasibility of Huawei, OPPO and other flagship models to sprint the high-end market.

2. Different user images. Dislocation competition can be called the usual tactics of the mobile phone market. Of course, the success of misplaced competition is judged according to the user's portrait.

iPhone user portraits are concentrated in first- and second-tier cities, and are mainly 19-39-year-old users; vivo users are mainly young users, mainly living in small and medium-sized cities below the third and fourth lines; Huawei P series is for male users. The main, Nova series has attracted a large number of women; Xiaomi is still the majority of male users, the highest proportion of young people aged 19-22. Interestingly, OPPO, iPhone's user set "food" and "buy buy and buy" in one, while Huawei, Xiaomi has more "workaholics", the dividing line between fashion and business is gradually clear.

3. Weibo social marketing has become “the king of goodsâ€. Marketing is an indispensable force for mobile phone sales, but the preference for marketing methods directly affects user composition.

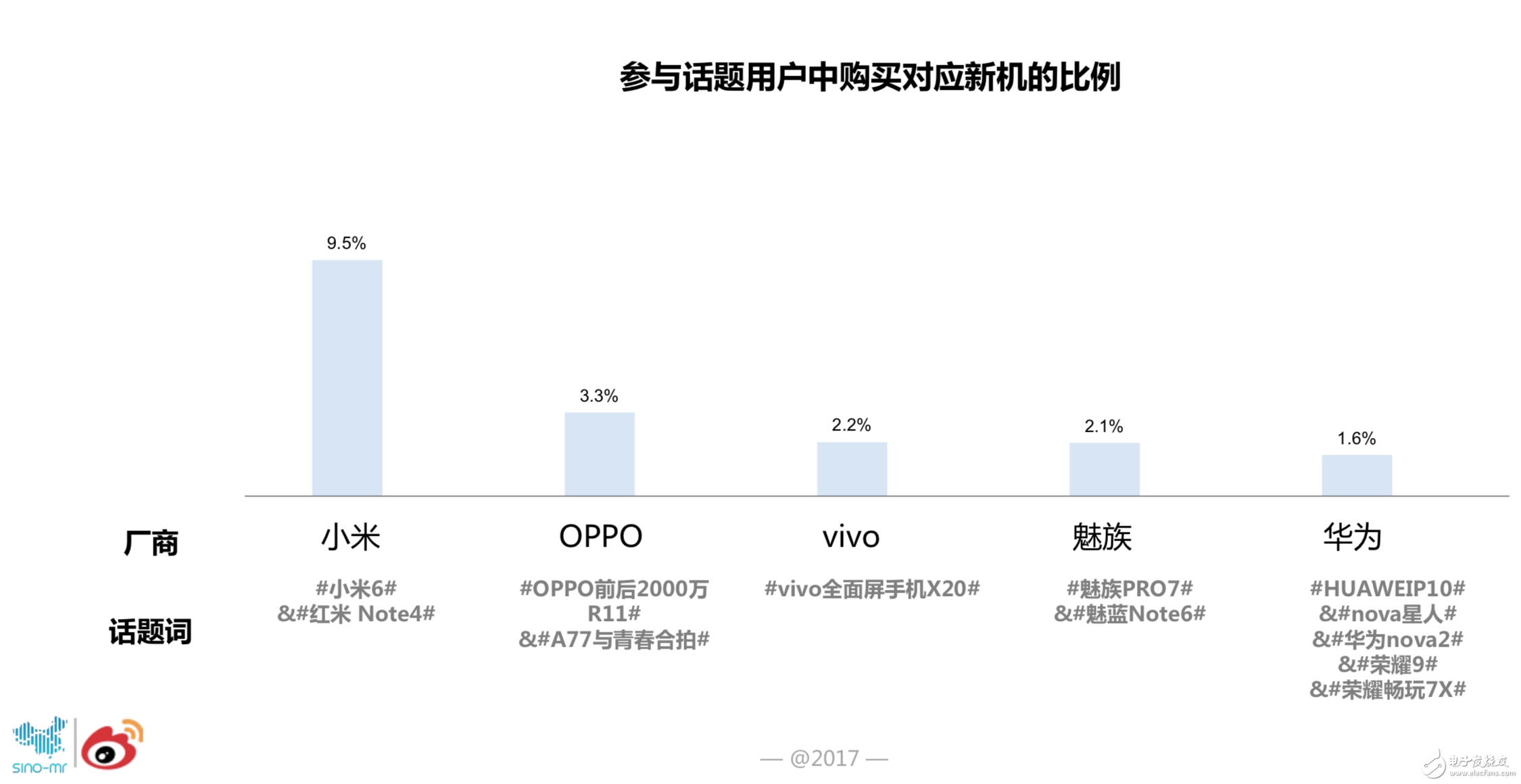

Xiaomi is a master of content operation. In the proportion of microblogging topics and new machine purchases initiated by major mobile phone brands, the conversion of Xiaomi is as high as 9.5%, much higher than 3.3% OPPO and 1.6%. Huawei. Judging from the choice of spokespersons, Chen Weijun, Li Yifeng, Lu Yi, Peng Yuxi and so on have successfully brought a large number of female users to OPPO and vivo. The use of Wu Yifan and Hu Ge's Xiaomi and Huawei has still failed to change the proportion of males. In view of the bottoming out of Xiaomi in 2017, the “capacity of goods†of Weibo’s social marketing is evident.

4. Performance degradation is still the main motivation for changing machines. The saying that there is a surplus of smartphones is endless, which greatly improves the user's replacement cycle, but the performance degradation is still the main motivation for the replacement.

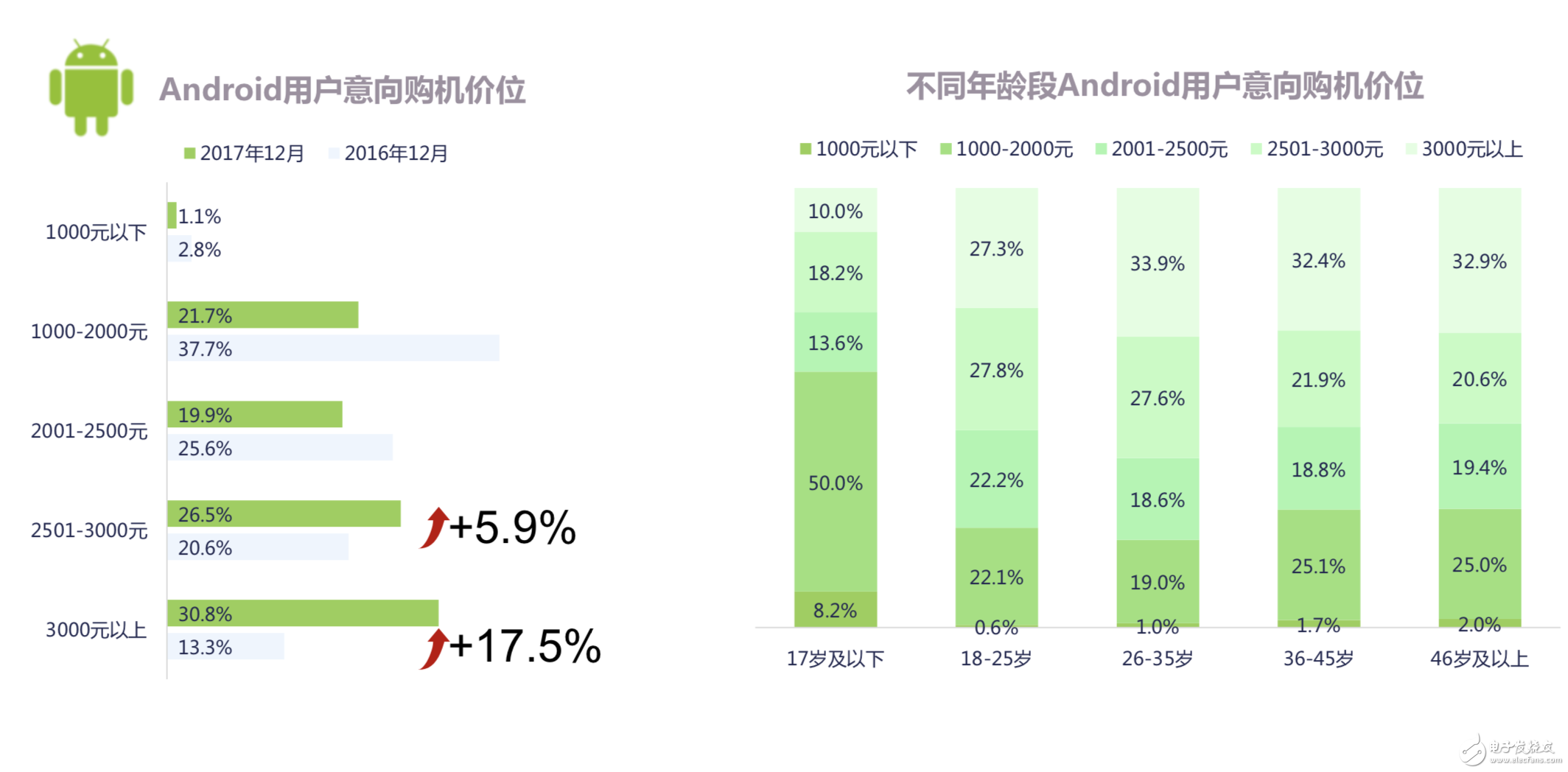

According to the data given by Weibo, the white-collar workers aged 26-35 are the mainstay of the replacement, and 58% of the users have used at least 5 smartphones. At the same time, the overall user replacement cycle continued to lengthen, and the number of users who changed the machine dropped to 8.6% in one year, and nearly 50% of the users changed their machines in two years. The growth of the replacement cycle may not be a complete bad news. Users have greater demand for performance, resulting in a 5.9% year-on-year increase in products at the price of 2,500-3,000 yuan, and a year-on-year increase of 3,000 yuan or more. .5%, the sensitivity to price is further reduced.

5, the user's pain points show diversity. Different user pain points are the key to the dislocation competition in the mobile phone market, and it is also the only way for mobile phone manufacturers to create differentiation.

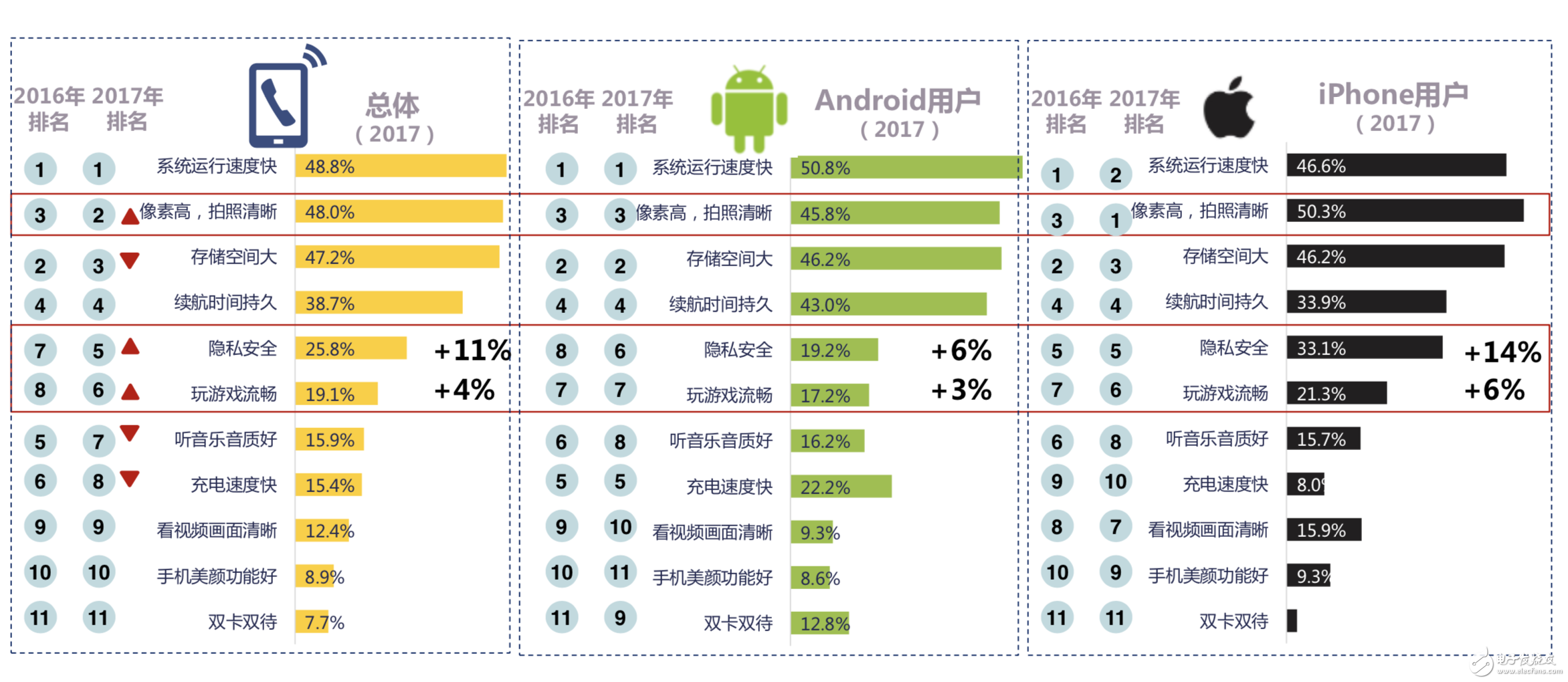

In addition to the popularity of system fluency, battery life, storage space and other pain points, the impact of photos, privacy, and games on user decisions has further expanded. Almost all mobile phone brands are working hard to take pictures. After 2018, artificial smart photography has gradually become mainstream, but privacy points such as privacy and games still need to be further satisfied. Although some mobile phone manufacturers have begun to pay attention to cloud services and security protection, they have begun to work on GPUs. The CPU optimization provides a good gaming experience, and it is still lacking at present.

Who will be eliminated if they leave the user?

4.11 billion live Weibo, perhaps the data is only "what mobile phone is used by people who play Weibo", and "What are the characteristics of these users", but Weibo is up to 93% of mobile users, quite accurate The feedback on the market performance of different mobile phone brands.

From the macroscopic perspective, the mobile phone industry chain is becoming more and more mature, and the terminal users are becoming more and more mature. The oligopoly competition is an inevitable trend and an inevitable performance of the market maturity. Why is there a small number of brands against the trend when the overall market declines? The "Smart Phone Micro Report 2017" made a short reply: Whoever is separated from the user will be eliminated by the user and eventually forgotten by the user.

The Android P released three months ago has added an app called “Dashboard†that can display the duration of each app. The value may not be “anti-addictionâ€, but a record of the track used by the user APP. Coincidentally, the newly released iOS 12 also added the "Digital Health" feature to help users manage the time spent on the iPhone and iPad, and show in detail how long each app is used. It can be guessed that research based on user behavior will gradually become mainstream and become the vane of competition in the mobile phone market.

Social networks such as Weibo record the user's emotional behavior, such as what type of movie the user likes, what brand of cosmetics to use, what type of game to play, where to hack, and where the user changes direction. For the fiercely competitive mobile phone market, how to accurately find the brand audience, how to meet the user's differentiated demands, and thus judge the next trend of the mobile phone industry, the social platform has long been an indispensable channel.

The more positive cases may be new oligarchs such as Huawei, OPPO, vivo, and Xiaomi. Huawei has seized mature business users and is also vying for young users with sub-brands such as Nova and Glory or independent brands; OPPO and vivo users are concentrated in third- and fourth-tier cities, but OPPO is also passing offline activities, super Flagship stores and other brands to expand the influence of first- and second-tier brands, while OPPO Find X, vivo NEX, etc. released signals to adjust product layout; Xiaomi already has loyalty far higher than other brands, and constantly rely on social operations to enlarge this A trend.

Apple and Samsung have actually played a role in the Chinese mobile phone market. The appeal of iOS to Android users continues to decline. Although Samsung's global shipments have picked up, it has not stopped slipping in the Chinese market. There are some accidental factors, such as Samsung's high-end image in the market, it should be the iPhone's most important "taker", in fact, the iPhone and Samsung's market share is gradually being eaten by the domestic giants. Is this not a destined result? Product positioning and user needs are out of touch, marketing and user behavior are out of touch, and the main service is out of touch with users.

Conclusion

The data analysis of GFK has made the prediction of the siphon effect in the domestic mobile phone market. The market share of the head brand is expanding, but the survival space of small and medium-sized manufacturers is becoming less and less. Correspondingly, Jin Li's long-term capital chain break crisis, Meizu, Motorola and other layoffs, as well as Samsung, Apple and other unsatisfactory in the Chinese market. When the inverted pyramid structure disappears, "medium life" and so on are facing the torment of winter.

The data reflects the performance of market competition, and user behavior reflects the way of thinking of different mobile phone brands. At least the head brands have established a sense of “winners eat allâ€. If the second and third line brands still believe in the natural distribution of traffic, the giants take 50%, and their own total is 20% or 30%. Forgetting will be the result of the doom. After all, the rules of the numbers are out of place, but the user behavior is not deceptive.

Htn Panel,Positive Transflective Lcd Display Module,Htn Monochrome Lcd Display,Htn 7 Segment Lcd Display

Huangshan Kaichi Technology Co.,Ltd , https://www.kaichitech.com